Why Bankruptcies Are Up: It’s the Economy, Stupid

James Carville’s old line still tells the truth for many Alaskans today.

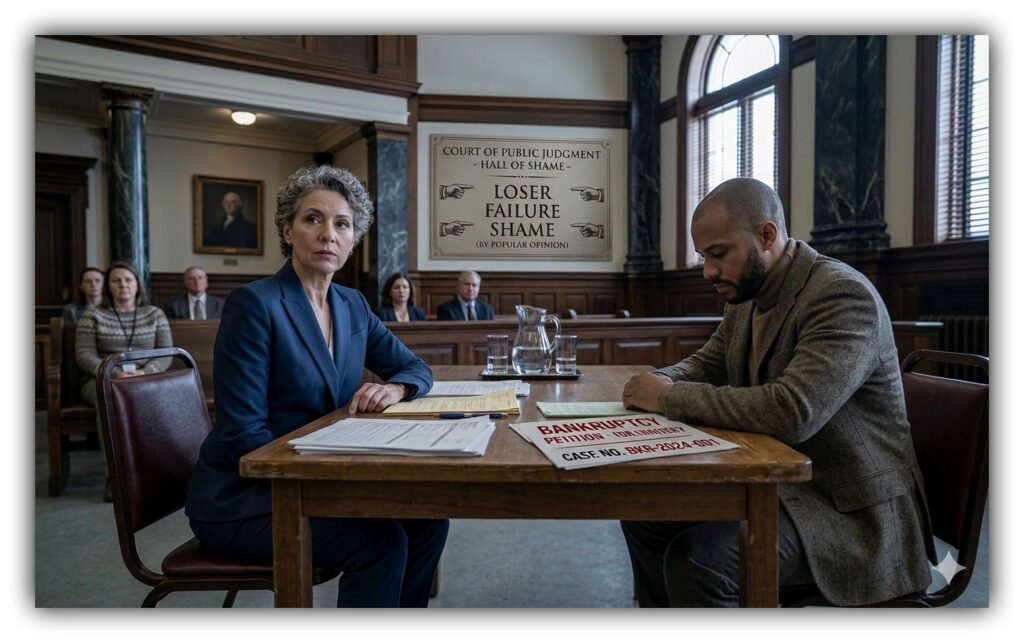

The Part of Bankruptcy No One Explains Until You’re Already There

By Gina Hill | Alaska Headline Living | April 23, 2026

Bankruptcies are rising again. Across the country, more people are filing, and the numbers are not just “normal business.” They are a sign that the economy is squeezing households in ways that are hard to ignore.

In Alaska, where groceries, gas, heating fuel, and housing already cost more than in many other states, the pressure is especially sharp. People are not filing because they suddenly “lost control.” They are filing because the economy has already pushed them to the edge.

That is the starting point of this story.

Bankruptcies Are Up. Why?

The U.S. Courts reported 591,850 total bankruptcy filings for the 12‑month period ending March 31, 2026, an increase of 11.9 percent from the previous year. That jump is not random. It lines up with a broader squeeze on everyday life.

Credit card debt is harder to carry when interest rates stay high. Housing costs have not come down. Medical bills keep piling up. National trends play out in Alaska in a familiar way: as prices rise, paychecks barely budge, and people start running out of places to cut.

When transportation costs rise, everything else follows. Goods cost more to move. Everyday essentials creep up. Family budgets tighten in ways that are hard to escape.

It is rarely one crisis. It is several at once.

The Same Economy, Very Different Experience

Even though everyone is in the same economy, bankruptcy does not land the same way for everyone. That is the hidden part people rarely talk about.

For many regular people, bankruptcy is not a “tool.” It is something they have been taught to avoid at all costs. It is seen as a sign of failure, personal irresponsibility, something to be ashamed of. That stigma can delay action, sometimes for years, until the situation becomes legally unavoidable.

By contrast, the wealthy and big businesses often frame bankruptcy as “financial restructuring.” They use it to shed debt, reorganize contracts, or change their balance sheet. It is treated as a business decision, not a moral failing.

Same legal system. Same rules. Very different story.

The Hidden Cost of Stigma

The stigma around bankruptcy shapes behavior long before anyone walks into a courtroom.

The shame of financial failure often feels heavier than the debt itself. Many people wait until they are at a breaking point before they seek help. Advocates are working to make clear that bankruptcy is a legal tool for a fresh start, not a reflection of character. | Alaska Headline Living ©

People who treat bankruptcy as a tool tend to seek legal help early, talk to creditors, and file before things fully collapse. They are more likely to negotiate payment plans, restructure, or use Chapter 11 or Chapter 13 to stay in control.

People who see bankruptcy as failure tend to wait, try to hold on, and only file once collections notices, wage garnishments, or eviction threats are already in motion. By then, their financial picture is often more damaged and harder to repair.

Same law. Very different starting point.

Why Timing Matters

Bankruptcy does not begin on the day someone files. It begins much earlier, while people are still trying to keep up. It is the month you decide which bill gets paid first. It is the week you skip something else to cover rent, gas, or groceries. It is the quiet stress of trying to stretch a paycheck that no longer stretches far enough.

In Alaska, where seasonal income, long winters, and high fuel and food costs are everyday realities, that pressure hits earlier and harder. By the time someone files, their situation may look nothing like another person’s case. One person may already be dealing with collections, closed accounts, or eviction risk. Another may still have room to negotiate or plan ahead.

Same system. Same paperwork. Very different path.

What Happens When the Economy Is the Real Problem

Even within one legal process, bankruptcy does not produce one outcome. Some people discharge most unsecured debt and rebuild faster than expected. Others enter long repayment plans or lose assets along the way. What changes the outcome is not just the law, but what someone is carrying into the process, financially and emotionally, and how early they feel safe enough to act. For many Alaskans, that includes the weight of stigma, the fear of being seen as a failure, and the sense that asking for help means giving up.

In Alaska, bankruptcy cases are handled through the federal court system. The U.S. Bankruptcy Court for the District of Alaska offers basic guidance, but for many people, the real barrier is not the paperwork. It is the feeling that asking for help means admitting failure.

That feeling is not accidental. It is part of a culture that treats bankruptcy as a “last resort” for ordinary people, while wealthy individuals and corporations quietly use it as a regular financial maneuver. The rest of the people struggle in the middle, watching the economy pull them down while the stigma makes it harder to reach for the tools that already exist.

If You Need Help

If this is where you or someone you know is, help exists before filing becomes the only option.

A lawyer, credit counselor, or advocate meets calmly with a client across a simple table piled with paperwork and a cup of coffee. This is what early help can look like before bankruptcy becomes the only option—quiet, practical, and focused on options rather than stigma. | Alaska Headline Living ©

- U.S. Courts Bankruptcy Basics

- Alaska Legal Help

- U.S. DOJ Approved Credit Counseling Agencies

- National Foundation for Credit Counseling

You do not have to wait until everything breaks to ask questions. The smartest move is often asking for help early, while you still have options on the table, so a lawyer, credit counselor, or advocate can walk you through what bankruptcy really means and whether there are steps you can take to avoid it altogether. Because as James Carville famously put it, “It’s the economy, stupid!” If the system is pushing ordinary people toward bankruptcy while the wealthy treat it as a routine financial tool, the problem is not you. It is the conditions you are living in.

Sources

- Administrative Office of the U.S. Courts, “Bankruptcies Increase 11.9 Percent,” U.S. Courts Data & News, April 23, 2026 (12‑month filings ending March 31, 2026, including total filings and breakdown by business and non‑business, and by chapter).

- U.S. Courts, “Historic Bankruptcy Caseload Statistics,” Tables F and F‑2, 2022–2026 (trend data by chapter and filing type).

- U.S. Courts, “Bankruptcy Basics” and Federal Rules of Bankruptcy Procedure (general overview of bankruptcy chapters and process).

- Federal Reserve Bank reporting on household debt and interest rate environment, 2025–2026 (context for credit costs and financial stress).

- U.S. Energy Information Administration and market reporting on oil price volatility tied to Middle East shipping disruptions in the Strait of Hormuz (fuel‑cost context).